2 hours ago

4

2 hours ago

4

The demand for critical energy transition materials such as copper, lithium and cobalt is on the rise due to the expansion of clean energy technologies. Credit: Unsplash/Lj. Filipović

The demand for critical energy transition materials such as copper, lithium and cobalt is on the rise due to the expansion of clean energy technologies. Credit: Unsplash/Lj. FilipovićUNITED NATIONS, July 2 (IPS) - Demand for critical energy transition minerals (CETMs) is expected to surge over the coming decades as countries expand clean technology capacity, develop electric vehicles, create battery storage, implement renewable energy systems, and introduce digital infrastructure according to UNCTADs latest report, The Shifting Dynamics of Critical Minerals Trade.

CETMs include lithium, nickel, cobalt, and rare earth elements, making them vital to producing low carbon clean energy alternatives and renewable technologies used for electricity production and battery storage. These elements are also commonly found within datacenters, semiconductors, consumer electronics, and any field requiring digitalization.

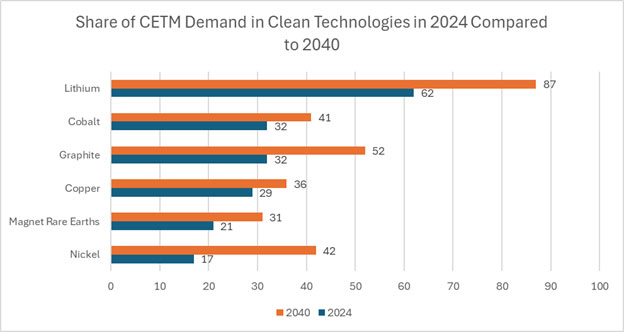

According to the report, demand for lithium is projected to increase by 353 percent by 2040, followed by graphite (131 percent), nickel (69 percent), magnet rare earths (65 percent), cobalt (49 percent), and copper (28 percent).

Naturally this surge in CETM demand also has changed the composition of where CETMs are being used, with clean technologies absorbing a growing share in the industry of CETMs.

Share of Critical Mineral Demand for Clean Technologies. Credit: Maximilian Malawista / IPS

Share of Critical Mineral Demand for Clean Technologies. Credit: Maximilian Malawista / IPSAlthough these CETMs are experiencing a surge in demand, from mining to processing or refining, the entire value chain is geographically concentrated between a few countries, dominating the entire global output. This same pattern also follows for reserves of key minerals, such as lithium, cobalt, nickel, and rare earth elements which are unevenly distributed among a few states.

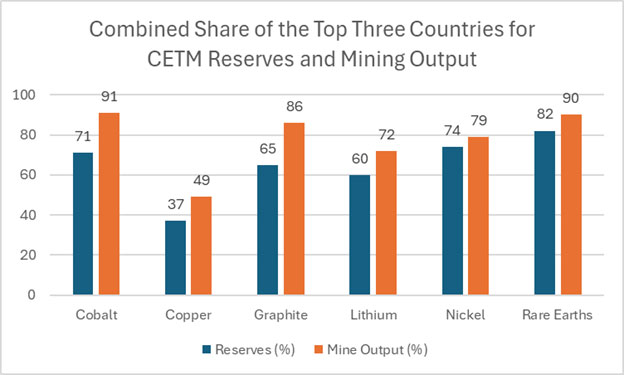

According to UNCTAD, China accounts for 69 percent of rare earth element production, and produces 78 percent of natural graphite capacity. Indonesia accounts for 67 percent of global nickel production, while the Democratic Republic of the Congo (DRC) accounts for 50 percent of global cobalt reserves and 47 percent of global cobalt mine production.

“Reserves” refer to mineral deposits which can be economically extracted using available technology, differing from total geological resources, which include deposits not yet commercially viable or known. Due to the situation of current reserves and mining output, only a few nations produce the majority of the capacity of critical minerals. The concentration of production and reserves leaves global supply chains highly vulnerable to geopolitical disruptions, and trade restrictions, among other shocks.

Represented is how much of the global reserves/mining output of CETMs is within just the top three countries. Credit: Maximilian Malawista / IPS

Represented is how much of the global reserves/mining output of CETMs is within just the top three countries. Credit: Maximilian Malawista / IPSNotably, mining output is slightly more concentrated than reserves for every mineral shown, indicating that mining production is controlled by an even smaller group of countries than the resource base itself.

This means that an overwhelming amount of these materials needed for some of the most critical functions for today and for our future rely on three countries for the entire global trade to function.

UNCTAD states: “Mining is capital-intensive and characterized by long lead times, limiting short-term supply responsiveness and leaving concentrated supply chains exposed to geopolitical risks, governance challenges, and environmental and social pressures.”

While the mining process receives much of the attention, UNCTAD argues in their report that refining represents an even larger vulnerability due to processing capacity being concentrated within a even smaller number of countries.

Refining and other downstream stages are even more concentrated” than that of mining, “creating critical bottlenecks in CETM supply chains,” An UNCTAD spokesperson told Inter Press Service. “A country may possess abundant mineral reserves yet remain dependent on a small number of foreign suppliers for refining, separation, precursor materials or advanced components.” They added explaining how there are “technical know-how, industrial capabilities, infrastructure and market power”, which means that “access to mineral resources alone does not necessarily translate into secure access to supply.”

UNCTAD also highlights that the concentration is also within only a few firms, in “several critical mineral markets” where a relatively small number of companies control “significant shares of mining, processing, trading, refining and technology.”

The issue as UNCTAD points out is that refining requires substantial long-term capital investment, access to advanced technologies, significant energy inputs, and specialized infrastructure, along with being an economy of scale to be cost competitive, which creates massive barriers to entry for new players.

Because global supply is concentrated, naturally international trade is the primary mechanism through which these minerals move between countries. The UNCTAD spokesperson remarked that “Cross-border trade in ores, concentrates, refined materials, and downstream components enables access to geographically dispersed stages of production across complex global value chains, particularly in high-technology sectors.”

What this means is that most countries depend on imports of CETMs at some point of their value chain for their manufacturing or developmental needs.

While diversification of processes would be necessary to alleviate risk associated with CETMs, since 2020 restrictive export measures on CETMs have been on the rise.

Mineral-rich economies like China, Indonesia, and the Democratic Republic of the Congo are seeking to capture higher value stages of production, rather than just exporting raw materials alone. Restrictive export measures are increasingly being introduced to capture more of the downstream value, encouraging domestic refining, industrial development, and manufacturing, rather than solely relying on commodity exports.

Of these measures, licensing requirements, export taxes, and exports bans make the most common measures.

Since 2020, 37 licensing requirements, 31 export tax measures, 29 export bans, and 1 export quota have been recorded. 18 of these export measures were implemented by the Democratic Republic of the Congo, with China introducing 16 followed by Indonesia at 12. Other countries such as Burundi and the Bolivarian Republic of Venezuela have introduced 8 measures each, while Zimbabwe has 7.

While at the moment supply chains are extremely concentrated and are becoming even further concentrated creating higher risk for importers, UNCTAD notes that major CETM importers such as the European Union, Japan, and the United States are adopting strategies to alleviate risk by diversifying import sources, increasing domestic capacity development, recycling, and developing strategic partnerships. In a three-year period, since 2022 such agreements in developmental stages have grown from just 15, to an addition of 58 new agreements targeting a diversification across value chains, and securing mineral access and production in a safe and future proof manner through policy.

As demand for CETMs accelerates, governments are increasingly looking at supply chains with scrutiny, seeing them as a strategic asset. While producing CETM high-capacity nations are seeking to control more value through domestic production of other stages and create more industry, major importers are moving aggressively to diversify supply sources to build more resilient supply chains. The outcome could not only decide the speed at which the global energy transition occurs, but also shape which countries will emerge as the key trading hubs and industrial powerhouses of the clean-energy economy.

IPS UN Bureau Report

© Inter Press Service (20260702075219) — All Rights Reserved. Original source: Inter Press Service